Call center software provider Five9 (NASDAQ: FIVN) beat Wall Street’s revenue expectations in Q1 CY2025, with sales up 13.2% year on year to $279.7 million. The company expects next quarter’s revenue to be around $275 million, close to analysts’ estimates. Its non-GAAP profit of $0.64 per share was 32.5% above analysts’ consensus estimates.

Is now the time to buy Five9? Find out in our full research report .

Five9 (FIVN) Q1 CY2025 Highlights:

Company Overview

Started in 2001, Five9 (NASDAQ: FIVN) offers software-as-a-service that makes it easier for companies to set up and efficiently run call centers to offer more tailored customer support.

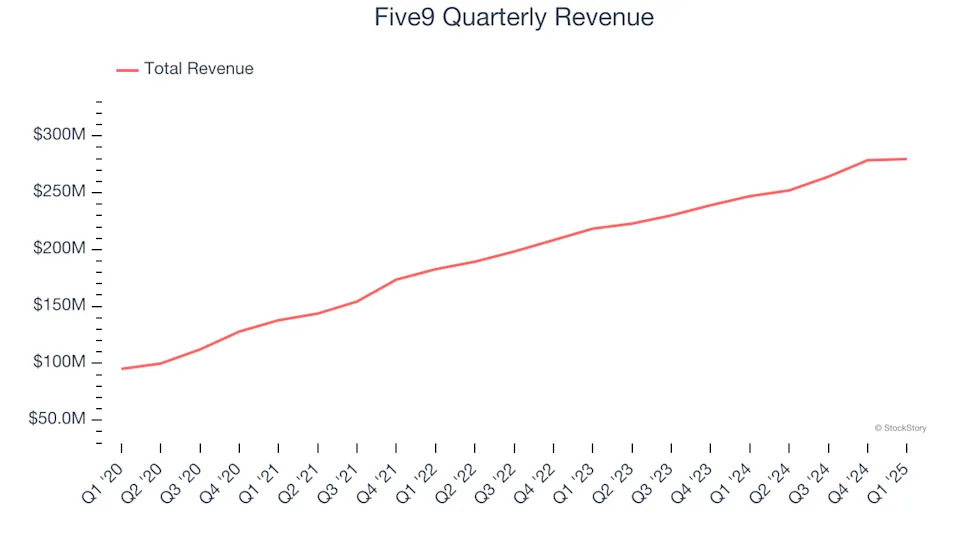

Sales Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last three years, Five9 grew its sales at a 18% compounded annual growth rate. Although this growth is acceptable on an absolute basis, it fell slightly short of our standards for the software sector, which enjoys a number of secular tailwinds.

This quarter, Five9 reported year-on-year revenue growth of 13.2%, and its $279.7 million of revenue exceeded Wall Street’s estimates by 2.6%. Company management is currently guiding for a 9.1% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 8.4% over the next 12 months, a deceleration versus the last three years. This projection is underwhelming and suggests its products and services will see some demand headwinds.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. .

Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

It’s relatively expensive for Five9 to acquire new customers as its CAC payback period checked in at 134.9 months this quarter. The company’s slow recovery of its sales and marketing expenses indicates it operates in a highly competitive market and must invest to stand out, even if the return on that investment is low.

Key Takeaways from Five9’s Q1 Results

We were impressed by Five9’s optimistic EPS guidance for next quarter, which blew past analysts’ expectations. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this quarter featured some important positives. The stock traded up 3.6% to $26 immediately after reporting.

Five9 put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free .